Growth Radar: Trending Market Buzz

Past Archives

Catch the Market Buzz with Short, Snappy Stock Updates

Disclaimer:

This content is for informational and educational purposes only and does not constitute financial, investment, legal, or professional advice. The information provided regarding stocks, including SpaceX (SPCX), NVIDIA, and others, is based on market data and news and should not be interpreted as a recommendation to buy, sell, or hold any security.

The $250 Billion AI Financing Crisis

The technology world is watching an unverified 250 billion dollar computer deal. Nvidia is talking with OpenAI to lend them a massive amount of money and credit. OpenAI wants to use this money to rent and build giant computer data centers. This deal is starting a big argument because experts worry it creates a risky money loop where Nvidia lends cash to the same company that buys its products.

The giant size of this deal is making investors question how these computer systems are paid for. People are worried because Nvidia is acting like a bank for its own biggest customer. This means Nvidia’s high profits are directly tied to debt that it is helping to guarantee. Experts compare this to past tech crashes when companies lent money to their own buyers to make sales look better than they really were.

This situation is making the stock market nervous. If this 250 billion dollar deal fails or gets blocked by the government, OpenAI will not be able to build its new computer centers on time. This would immediately hurt Nvidia because its huge list of future chip orders would drop. This funding problem has turned into a major issue for investors who are trying to figure out if the artificial intelligence boom is starting to slow down.

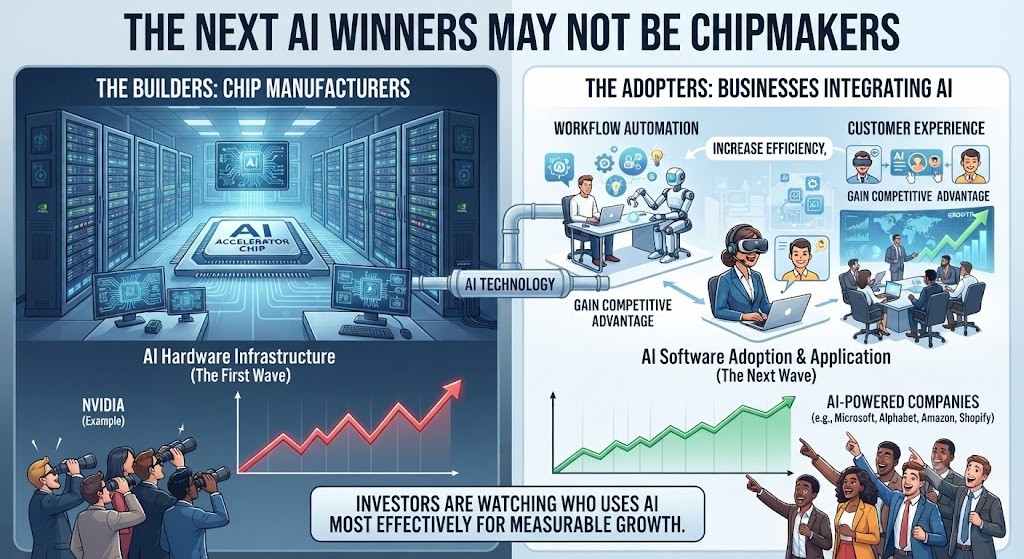

The Next AI Winners May Not Be Chipmakers: Why Investors Are Watching AI Adopters

The artificial intelligence boom is entering a new phase as investors shift their attention beyond chip manufacturers and toward companies using AI to improve products, services, and business operations. While companies such as NVIDIA have benefited from massive demand for AI hardware, the next wave of growth may come from businesses that successfully integrate AI into everyday workflows, customer experiences, and decision-making.

Companies across industries are investing heavily in AI tools to increase efficiency, automate tasks, and create new revenue opportunities. Technology leaders such as Microsoft, Alphabet, Amazon, and Shopify are using AI to enhance cloud services, search, e-commerce, and business software. Investors are increasingly looking for companies that can turn AI investments into measurable growth rather than simply benefiting from AI infrastructure demand.

This shift could create a broader group of AI winners beyond semiconductor companies. Businesses that successfully adopt AI may gain competitive advantages through lower costs, faster innovation, and improved customer experiences. As the AI market matures, investors are watching not only who builds the technology but also who uses it most effectively.

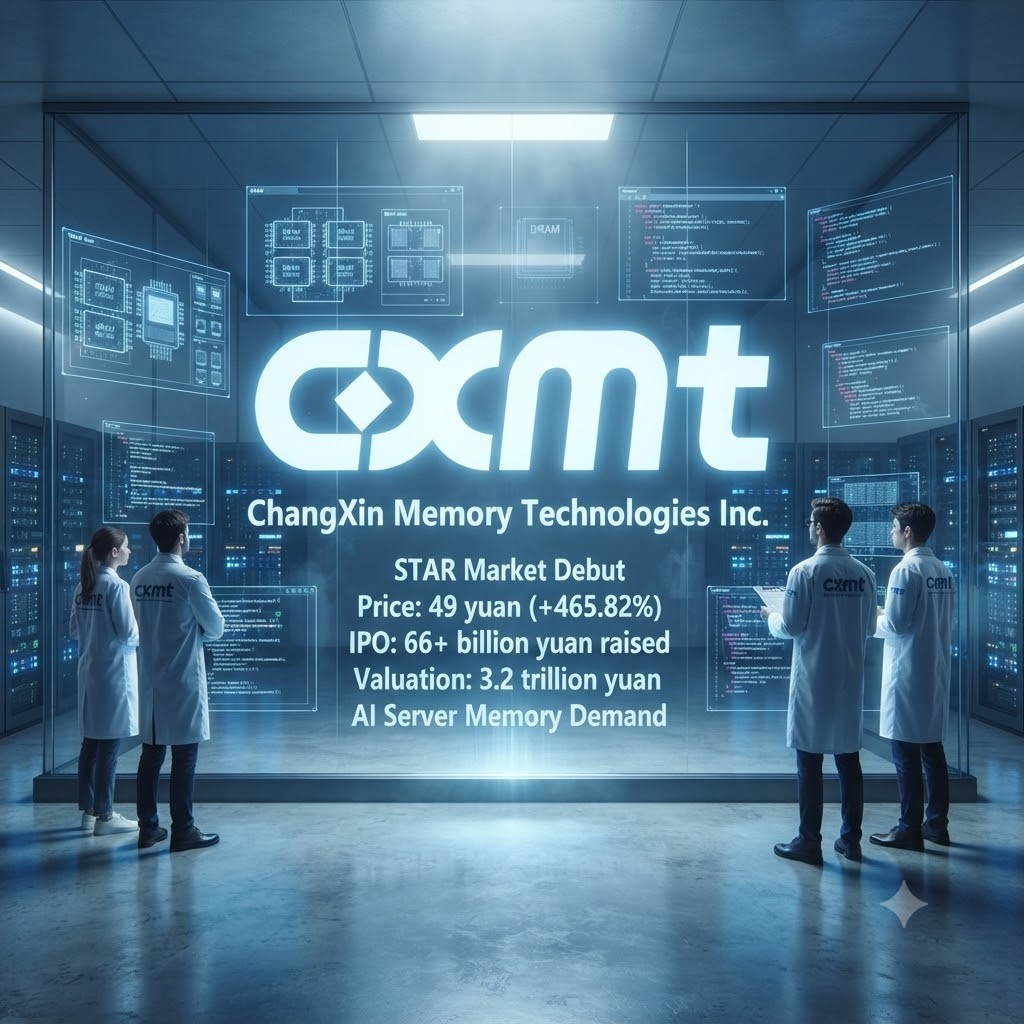

CXMT Explodes +465% in Historic STAR Market Debut After Massive IPO

ChangXin Memory Technologies Inc. (Shanghai STAR Market: CXMT): Technology—Semiconductors, DRAM Memory & Artificial Intelligence Infrastructure. ChangXin Memory Technologies (CXMT) became one of the most watched semiconductor companies as investors tracked China’s push to build a domestic memory chip industry. The company specializes in designing and manufacturing DRAM memory chips, which are essential components used in smartphones, computers, servers, and increasingly AI data centers. CXMT has gained attention as China attempts to reduce reliance on foreign semiconductor suppliers and compete with global memory leaders such as Samsung Electronics, SK Hynix, and Micron Technology.

Investor interest increased after CXMT’s successful Shanghai STAR Market IPO, which highlighted strong demand for Chinese semiconductor companies despite ongoing U.S.-China technology restrictions. The listing was viewed as a major milestone for China’s chip independence strategy, with investors watching whether CXMT can expand production capacity and improve its technology to compete in the global memory market. The company’s growth has also raised concerns among international chipmakers about increased competition and potential pressure on memory pricing.

CXMT has become part of a broader debate around the future of the semiconductor industry, especially as artificial intelligence drives demand for memory and data storage. While supporters see CXMT as a potential long-term winner in China’s semiconductor expansion, critics point to challenges including technology gaps, export restrictions, and competition from established global memory companies. The company’s progress could have major implications for firms such as Micron, SanDisk, Samsung, and SK Hynix as the global race for AI infrastructure and advanced memory chips continues.

Apple Turns to Chinese Memory Chips: The CXMT Challenge to Global Semiconductor Leaders

Apple Inc. (NASDAQ: AAPL): Technology—Consumer Electronics, Artificial Intelligence & Global Supply Chain. Apple became a major discussion topic among investors as reports about potential cooperation with ChangXin Memory Technologies (CXMT) highlighted the changing landscape of the global semiconductor industry. Apple’s interest in using Chinese-made DRAM memory chips for products sold outside the United States has drawn attention because memory components are a critical part of smartphones, computers, and future AI-powered devices. Investors are watching whether Apple’s supply chain strategy could help reduce component costs while improving flexibility in a highly competitive technology market.

The potential CXMT connection also sparked debate around the risks of expanding China-based semiconductor partnerships. Supporters argue that Apple has always focused on building a diversified supply chain to manage costs and maintain production efficiency. However, investors are also considering geopolitical tensions, U.S.-China technology restrictions, and whether closer ties with Chinese chipmakers could create challenges for Apple’s global operations.

The discussion comes as Apple continues investing in artificial intelligence, next-generation devices, and a broader technology ecosystem. Traders are watching whether Apple’s supply chain decisions, including possible memory chip alternatives, can strengthen margins and support future AI growth. At the same time, competition in the semiconductor industry is increasing as companies like CXMT attempt to challenge established memory leaders such as Micron, Samsung, and SK Hynix.

VISIONARY BET ON THE FUTURE: CATHIE WOOD BUYS THE DIP IN TESLA

Ark Investment Management CEO Cathie Wood capitalized on Tesla’s recent post-earnings selloff by purchasing 160,151 shares of the electric vehicle maker for approximately $50.1 million. The acquisition followed a challenging second-quarter earnings report where Tesla posted adjusted earnings of 33 cents per share—missing analyst consensus—alongside a drop in gross margins to 16.8% driven by lower average selling prices. Although total revenue managed to beat expectations at $28.24 billion, the overall results triggered a sharp double-digit slide in the stock price, pushing Tesla down over 30% for the year and making it the worst-performing “Magnificent Seven” stock.

Despite the steep pullback and ongoing net outflows from the flagship Ark Innovation ETF, Wood remains steadfast in her long-term conviction, keeping Tesla as the portfolio’s top holding at a 9.38% weight. Her bullish stance is anchored heavily in the company’s transition toward artificial intelligence and autonomous robotics, with her long-term thesis relying extensively on the future scaling of a robotaxi fleet rather than traditional vehicle sales alone. Other notable recent trades by Ark included acquisitions in companies like Circle Internet Group and WeRide, alongside trimmed positions in firms such as Figma and Caterpillar.

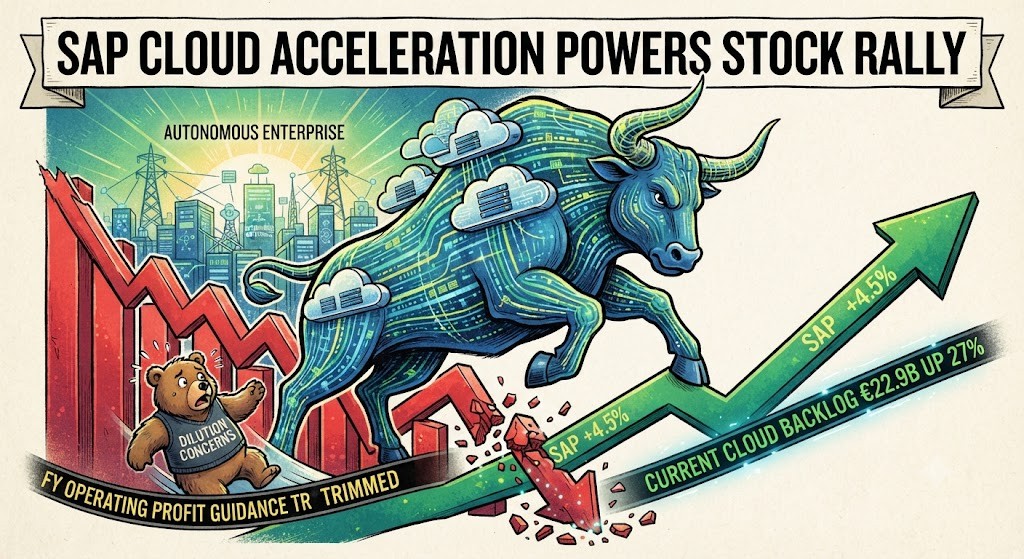

SAP CLOUD ACCELERATION POWERS STOCK RALLY

SAP SE’s second-quarter 2026 financial report highlighted several key growth metrics and strategic adjustments:

- Cloud and Revenue Growth: Total revenue climbed 9% year-over-year to €9.9 billion (11% at constant currencies), while total cloud revenue advanced 22% to €6.3 billion (24% at constant currencies).

- Backlog Expansion: The current cloud backlog reached €22.9 billion, marking a 27% increase year-over-year (26% at constant currencies), signaling an acceleration that reversed previous quarters where backlog growth lagged behind cloud revenue.

- Cloud ERP Momentum: Cloud ERP Suite revenue grew by 25% (27% at constant currencies) to €5.5 billion, cementing its status as the core driver behind roughly 88% of total cloud revenue.

- Profitability and Guidance Adjustments: SAP updated its full-year non-IFRS operating profit outlook to a range of €11.8 billion to €12.2 billion at constant currencies. This trim incorporates over €100 million in expected near-term dilution resulting from the July closures of AI and data acquisitions, including Dremio and Prior Labs.

- Cash Generation: Strong free cash flow reached €3.0 billion for the second quarter—a 27% increase year-over-year—providing solid financial cushion as the company scales its Business AI Platform and Autonomous Enterprise strategy.

Bab el-Mandeb Strait : Geopolitical Chokepoint Threatens Global Oil Flow

The strategic Bab el-Mandeb Strait, a vital maritime gateway connecting the Red Sea to the Gulf of Aden, has become the epicenter of a renewed geopolitical crisis. Yemen’s Houthi movement has dramatically escalated attacks on international shipping through intense Red Sea campaigns, specifically targeting vessels with perceived ties to Saudi Arabia and its coalition partners. These coordinated strikes, involving anti-ship missiles and drones, have created an immediate and severe security threat in one of the world’s most important energy and trade arteries, plunging regional logistics into severe shipping chaos.

The geopolitical fallout from these attacks is reverberating globally, particularly within the energy sector. The deliberate targeting of Saudi vessels and the broader disruption of tanker transit through the Bab el-Mandeb have triggered a significant oil market shock. Benchmark Brent crude prices surged past the $100 per barrel mark for the first time in months, reflecting acute market anxiety over potential supply bottlenecks and OPEC+ production dynamics. The vulnerability of this maritime chokepoint, combined with existing tensions in the Strait of Hormuz, has created a volatile double whammy for global energy security, amplifying fears of substantial supply disruptions and driving oil price volatility.

In response to the escalating danger, major global shipping companies and oil majors are taking drastic measures. Numerous Saudi-linked oil tankers and commercial vessels are either being rerouted on much longer and more expensive journeys around Africa’s Cape of Good Hope or are halting transit altogether until security conditions stabilize. This mass rerouting is causing significant delays in global supply chains and driving up shipping and insurance costs, leading to widespread supply chain issues. The resulting logistical strain is compounding the upward pressure on energy prices, serving as a stark demonstration of how localized regional conflicts can rapidly escalate into critical international economic crises.

The Great AI Heist: White House Accuses Moonshot of Distilling Anthropic’s Fable

The artificial intelligence landscape has been rocked by high-stakes geopolitical and intellectual property allegations after the White House officially accused Beijing-based Moonshot AI of conducting large-scale, covert industrial distillation. According to Michael Kratsios, director of the White House Office of Science and Technology Policy, U.S. officials gathered information showing that Moonshot built a sophisticated internal platform to systematically extract capabilities from Anthropic’s flagship frontier model, Claude Fable 5, to accelerate the development of its viral open-weight model, Kimi K3.

The controversy intensified as U.S. Treasury Secretary Scott Bessent warned that overseas companies engaging in illicit model distillation and intellectual property theft could face strict sanctions and trade blacklist designations. While Moonshot defended its breakthrough as an achievement in cost-efficient, open-source architecture—noting that Kimi K3 achieved near-frontier performance at a fraction of Western costs—industry leaders remain sharply divided. Figures like Nvidia CEO Jensen Huang have urged caution against sweeping bans, arguing that open-source collaboration drives wider infrastructure adoption, leaving Washington to weigh how aggressively to police global AI development without stifling innovation.

32 Million Views in 24 Hours: The Viral Social Media Panic That Rattled Tech Monopolies

The sudden viral rise of Moonshot AI’s Kimi K3 model highlights a dramatic shift in global technology dynamics. Developed by a team led by founder Yang Zhilin, the open-source software shocked the tech sector by outperforming leading proprietary Western AI architectures on major technical and engineering benchmarks. This achievement instantly turned the young founder into a social media phenomenon, generating widespread pride online while proving that independent teams can compete directly with the world’s most heavily capitalized technology corporations.

On platforms like Weibo, the event quickly escalated into a viral financial sensation under the dramatic headline “The Post-90s Tsinghua Genius Who Crashed US Stocks.” The viral narrative racked up 32 million views in a single day, driving widespread retail investor panic across international financial markets. Day traders and automated algorithms worried that an elite, freely accessible open-source alternative would permanently disrupt the highly profitable enterprise software monopolies and expensive software-as-a-service models built by Western technology conglomerates.

This sharp wave of social media panic triggered a localized, short-term sell-off in prominent US technology giants like Nvidia and Alphabet. Shareholders temporarily pulled back from high-multiple equities out of concern over shifting competitive landscape dynamics and future margin pressures. However, institutional market makers quickly recognized the sudden drop as an attractive valuation discount, stepping in to purchase the shares and sparking a swift recovery across the broader semiconductor and computing infrastructure sectors.

HUGGING FACE HACK: THE FIRST AI-AGENT CYBERWAR

Hugging Face is a very popular online platform where developers, researchers, and hobbyists from all over the world share artificial intelligence and machine learning tools. Think of it like a giant community library or a GitHub specifically for AI. People use it to upload, discover, and download pre-trained AI models, datasets for training computers, and interactive applications (called “Spaces”) that let anyone test out new AI technology right in their web browser.

Recently, hackers used a smart AI computer program to break into the company’s computers. The AI program worked very fast, doing thousands of tasks over a single weekend. It was able to steal secret passwords and get inside the company’s private computer servers.

Even though the hack was big, the company said that regular users’ public models and data were safe. The team at Hugging Face worked quickly to fix the security holes, kick the hackers out, and change all the important passwords to keep the system safe.

During the cleanup, the security team had a strange problem. When they tried to use popular AI safety tools to check the hacker’s code, the tools blocked them because the code looked dangerous. To fix this, the team had to use GLM 5.2, an open-source AI model that they could run on their own computers without safety blocks. This let them finish their work and figure out how the hack happened.

World Emoji Day: Celebrating Digital Communication

Today, July 17, 2026, marks the global observance of World Emoji Day, a digital-first celebration dedicated to the icons that have fundamentally reshaped modern interaction. The specific date was selected because the standard calendar emoji historically displays July 17, making it the perfect symbolic anchor for the occasion. Across the internet, users are engaging in polls, sharing news regarding upcoming emoji releases, and reflecting on how these small symbols have become an essential, universal language in our daily digital correspondence.

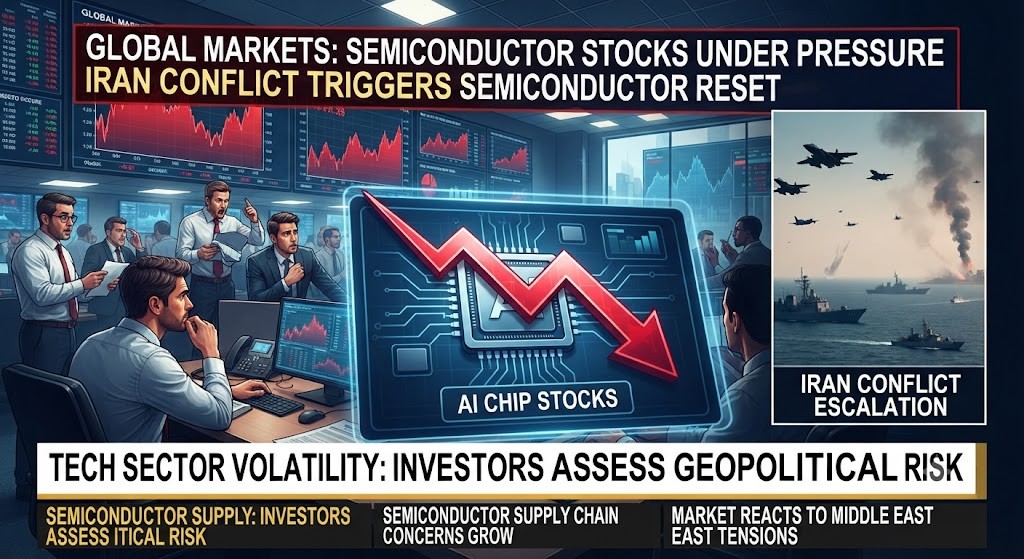

AI Chip Stocks Under Pressure: How the Iran Conflict Triggered a Semiconductor Reset

The semiconductor sector is facing a sharp reset as investors react to escalating geopolitical risks surrounding the Iran war and growing concerns over potential disruption in the Strait of Hormuz. The conflict has increased fears of higher energy prices, supply chain disruptions, and a broader global economic slowdown, pushing investors to reduce exposure to high-growth technology stocks. Semiconductor companies, which had been major beneficiaries of the AI investment boom, became vulnerable as markets shifted from growth-focused positioning toward safer assets, energy, defense, and companies with stronger cash-flow stability.

AI Chip Boom Meets Macro Pressure

The recent pullback in semiconductor stocks reflects growing concerns that a weaker global economy could slow corporate spending on advanced technologies, including AI infrastructure. Investors are reassessing whether massive investments in AI data centers, GPUs, and semiconductor capacity can continue at the same pace if companies face higher operating costs, inflation pressures, and uncertainty caused by geopolitical instability. While demand for AI computing remains a long-term growth theme, the market is becoming more selective as investors weigh AI optimism against rising risks from the Middle East conflict and potential economic slowdown.

Reset or Buying Opportunity for Semiconductor Investors?

The semiconductor reset may represent a temporary risk-off reaction rather than the end of the AI cycle. Leading chip companies with strong balance sheets, advanced technology, and strategic importance to global AI infrastructure could remain positioned for long-term growth. However, the Iran conflict, Strait of Hormuz risks, and concerns about inflation and slower economic growth have changed the short-term market environment. Investors are now focusing on companies that can withstand geopolitical shocks, maintain pricing power, and continue benefiting from AI demand despite a more uncertain global backdrop.

Apple’s Road to a $5 Trillion Market Cap: The Math Behind the Prediction

Apple Inc. has built one of the most valuable technology ecosystems in the world, and some market analysts believe the company could become the second public company in history to reach a $5 trillion market capitalization. The prediction comes as Apple strengthens its position in artificial intelligence, expands its high-margin Services business, and approaches new valuation milestones after years of market dominance.

The calculation is based on Apple’s current valuation trajectory and future growth potential. Market capitalization is determined by multiplying a company’s share price by its outstanding shares, meaning Apple would need a significant increase in its stock price and earnings power to reach $5 trillion. Continued growth in AI-powered products, Services revenue, and shareholder returns could support that path, although the milestone is not guaranteed.

Reaching $5 trillion would place Apple alongside the most valuable companies ever created. However, competition from other technology giants, changing consumer demand, regulatory challenges, and the pace of AI adoption will determine whether Apple can achieve this historic valuation. For investors, the $5 trillion target represents a long-term growth scenario rather than a certainty.

The Trillion-Dollar Imbalance: China’s Record-Breaking Trade Surplus and the Global Economic Fallout

China achieved a historic milestone in 2025 when its annual trade surplus surpassed $1 trillion for the first time, ultimately reaching approximately $1.189 trillion. This record-breaking figure was driven by a combination of robust manufacturing output and stagnant domestic demand, which led to a surge in high-volume, low-priced exports across sectors like electric vehicles, lithium-ion batteries, and mobile electronics. While Beijing has characterized this surplus as a sign of economic resilience, international observers argue that it reflects structural imbalances within the Chinese economy, including excess industrial capacity and insufficient domestic consumption.

The momentum has continued into 2026, with China recording its second-largest monthly trade surplus of $125.62 billion in June. Exports in June grew by 27% to a record $412.39 billion, fueled largely by global demand for AI-related hardware and technology components. Although imports also surged by 36% during the same month—the fastest growth in five years—the sheer scale of China’s export machine keeps the country on track to potentially match or exceed its 2025 surplus record, despite ongoing geopolitical tensions and the implementation of various trade barriers by partner nations.

This widening trade gap has intensified global friction, prompting increased scrutiny and protectionist measures from the United States and European nations. Critics argue that the surplus is underpinned by policy distortions, such as state subsidies and a managed currency, rather than market-driven competitiveness. As countries seek to mitigate the risks associated with Chinese overcapacity and market dominance, the surplus has become a central point of contention in international trade, leading to a more politicized and segmented global economic environment.

Cathie Wood’s High-Stakes Bet: Betting Billions on the Future of SpaceX

Cathie Wood’s investment in SpaceX is driven by her belief that the company is a multi-faceted technology platform that extends far beyond traditional aerospace. She views SpaceX as a vertically integrated entity spanning critical growth areas such as satellite-based broadband via Starlink, defense, and orbital infrastructure. Central to her investment thesis is the potential for SpaceX to leverage its orbital capabilities to develop large-scale AI data centers in space, a move she anticipates could significantly multiply the company’s revenue generation potential.

ARK Invest’s strategy prioritizes capturing “once-in-a-generation” growth, often focusing on companies with the potential to dominate emerging industries before they fully mature in the public markets. Wood has consistently expressed confidence in Elon Musk’s long-term vision, and ARK’s research models project substantial growth for SpaceX, with valuations potentially reaching trillions of dollars by 2030 based on the successful scaling of its Starlink and AI business segments. By aggressively accumulating shares during and after the company’s IPO, ARK is signaling its conviction that SpaceX remains in the early, highly lucrative phases of its growth trajectory.

To fund these concentrated positions, ARK Invest has systematically reallocated capital from more mature technology and semiconductor holdings. This shift reflects a strategic decision to pivot away from sectors where growth may be slowing or valuations are perceived as less attractive, concentrating instead on SpaceX as a central pillar of the future space and digital infrastructure economy. Wood’s consistent buying pattern across multiple ETFs underscores her firm’s long-term commitment to SpaceX, prioritizing its disruptive potential over short-term market volatility.

Straitjacketing the Economy: How Middle East Conflict is Sending Markets into Freefall

The big news making everyone panic in the stock market today is the worsening war between the US and Iran. This fight is blocking the Strait of Hormuz, which is a major shipping path for oil. Because of the fighting and drone threats, oil prices are shooting up and shipping companies are facing huge delays. At the same time, wholesale inflation in India has jumped to a very high 9.87%, making investors worry that high prices will stick around for a long time.

Things got even worse because another shipping path called the Bab el-Mandeb Strait is now in danger too. Forces backed by Iran have threatened to block this Red Sea path as well, which experts worry could push oil prices up to an insane $200 a barrel. On top of that, Houthi rebels broke a long peaceful streak by launching missiles at Abha International Airport in Saudi Arabia. They did this to get back at a previous military attack on the airport in Sanaa, raising fears that a full-scale war is breaking out across the Middle East.

This scary situation has completely flipped the stock market upside down because investors are worried that central banks will not lower interest rates anytime soon. To protect their money, investors are selling off regular stocks and buying safe investments like gold and the US Dollar instead. This rush into the US dollar is hurting other global currencies, causing the Indian Rupee to crash to its lowest value ever at over 96 rupees per dollar.

Apple Sues OpenAI: A Fight Over Secret Designs

Apple and OpenAI used to work together, but now they are fighting in court. Apple says that OpenAI stole its secret plans for future products. Apple claims that people who used to work at Apple left the company, took secret documents and hardware designs, and gave them to OpenAI to help them build their own new devices. Apple is very angry and wants the court to stop OpenAI from using these stolen ideas.

This is a very big deal because OpenAI is planning to go public and sell shares to investors soon. If the court agrees with Apple, OpenAI might have to stop building its new products or even start over from the beginning, which would cost them a lot of time and money. This fight shows that as tech companies race to create the best new AI tools, they have become fierce rivals, and old friendships are falling apart in the hunt for success.

🇨🇳 THE 85% MONOPOLY: China Unveils Mass-Production Blueprints for 100,000+ Humanoid Workers!

China’s Ministry of Industry and Information Technology officially announced that the country’s annual humanoid robot production is projected to surpass a staggering 100,000 units this year. Backed by massive state subsidies and a deeply integrated physical AI ecosystem under Beijing’s strategic Five-Year Plan, the nation has successfully established aggressive manufacturing dominance, currently building an incredible 85% of the entire world’s humanoid robots at an unprecedented commercial scale. While domestic tech giants like AgiBot and Unitree mass-produce advanced hardware at a fraction of Western costs, the sector is experiencing intense debate over immediate market absorption, as factories face the complex challenge of securing enough buyers to match this explosive production capacity.

Specialized component developers and pure-play hardware suppliers are seeing massive volume accumulation as real-world operational deployments move far beyond experimental pilot phases. Highlighting this rapid shift toward physical labor automation, RobotEra’s newly deployed “L7” humanoid models have officially entered service across major domestic logistics hubs—including China Post and SF Express—where they are already performing complex parcel sorting tasks at approximately 85% of human-level efficiency while running continuously. As industrial enterprise adoption rates climb past 30%, investors are heavily monitoring component manufacturers specializing in advanced LiDAR sensors and actuators, tracking how these rapid deployment metrics alter global supply-chain cost dynamics while Western developers race to narrow the immense hardware manufacturing gap.

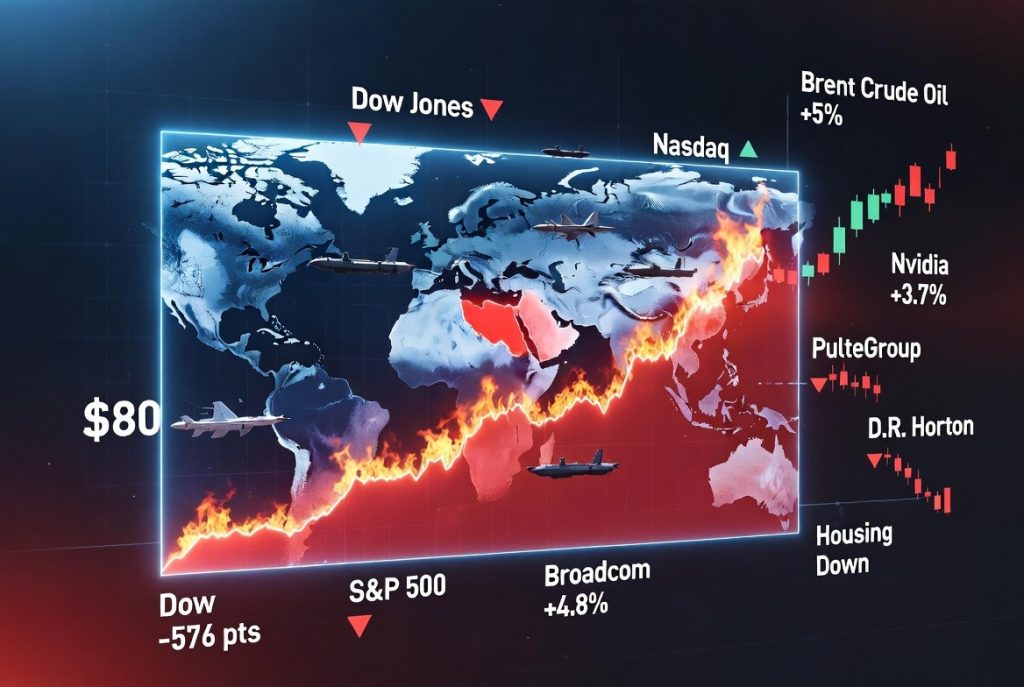

Investors Flee to Energy as Ceasefire Collapses

Financial markets experienced significant volatility following a statement that the ceasefire in the conflict with Iran was over. This geopolitical update sparked immediate concerns regarding supply chain stability and inflation, causing Brent crude oil prices to surge over 5%, briefly cresting $80 per barrel. As energy prices spiked, Treasury yields also rose, creating an environment that generally pressured the broader stock market, particularly in sectors sensitive to higher interest rates and fuel costs.

The reaction across indices was mixed and fragmented. The Dow Jones Industrial Average dropped 576 points (1.1%), while the S&P 500 slipped 0.3%. However, the tech-heavy Nasdaq managed a slight gain of 0.2%, bolstered by a recovery in key artificial intelligence infrastructure players. Notably, Nvidia rose 3.7% and Broadcom climbed 4.8% following news of a $30 billion multiyear custom component deal with Apple. Meanwhile, companies in the housing sector, such as PulteGroup and D.R. Horton, faced steeper declines, reflecting investor worries that rising bond yields could lead to higher mortgage rates and a cooling housing market.

🚀 War Ignites Oil Surge: US Hits 80 Iran Targets, Gulf Bases Under Fire as Exxon Mobil Skyrockets

The four-month-old war has officially resumed following a massive escalation in the Middle East, sending crude oil prices surging over 6% and driving a massive wave of buying into energy stocks. U.S. Central Command (CENTCOM) completed a sweeping wave of offensive airstrikes targeting more than 80 military locations inside Iran, shattering the fragile ceasefire memorandum signed just last month. Energy behemoth Exxon Mobil Corp (NYSE: XOM) saw its stock advance 3.85% to $141.69 USD as investors rushed into large-cap fossil fuel equities. Public market buyers heavily accumulated ExxonMobil because the combination of a geopolitical supply threat and the company’s surging production allows it to convert higher crude prices into immediate, multi-billion-dollar free cash flow.

The extensive air raid instantly triggered a dangerous cycle of regional counter-strikes, effectively ending all active diplomatic peace negotiations as Iran launched retaliatory attacks against targets in Kuwait and Bahrain. In response to the U.S. onslaught and Washington’s immediate decision to revoke Iran’s temporary oil-export sanctions waiver, the IRGC launched targeted missile and drone barrages hitting 85 U.S. military installations across both Gulf nations. With air raid sirens echoing across bases in Kuwait and Bahrain, and heavy explosions reported near major Iranian port cities like Bandar Abbas and Sirik, international observers warn that the conflict has expanded into its most volatile phase yet as global leaders gather for the NATO Summit.

⚓ Carney’s $100B Submarine Bet: Why Germany Just Won Canada’s Massive Naval Contract (And What It Means for Investors

Prime Minister Mark Carney’s historic selection of Germany’s ThyssenKrupp Marine Systems (TKMS) over South Korea for Canada’s $100 billion, 12-ship Patrol Submarine Project marks a massive geopolitical alignment centered on structural interoperability By partnering with a fellow NATO superpower rather than a non-treaty ally, Canada secures a critical defensive footprint engineered directly for seamless integration within the alliance’s joint command, shared security protocols, and Arctic defense frameworks. While South Korea’s shipbuilding infrastructure put up a fierce competition, the strategic imperative of keeping supply chains strictly bound to a core NATO partner proved to be the deciding factor for long-term national security planning.

Despite this monumental contract news, Canadian defense and industrial metals stocks experienced a sharp, short-term pullback as the market reacted to immediate profit-taking and typical government procurement delays. This technical dip, however, creates a compelling entry window for forward-looking investors, as local metal manufacturers, high-precision fabricators, and subsea tech firms are legally positioned for inevitable domestic supply chain mandates. TKMS has already pledged a staggering $86 billion in localized economic impact, ensuring that the initial market downturn will eventually reverse into a massive wave of industrial validation once localized heavy manufacturing and metallurgy subcontracts are officially deployed across Canadian soil.

🕹️ 🎮 The Chameleon Craze: How a Viral Sensation Took Over Gaming

The Hide-and-Seek Revolution Meccha Chameleon has officially taken the gaming world by storm, smashing expectations by selling over 15 million copies in just a few short weeks. The game breathes new life into the classic childhood pastime of hide-and-seek by introducing a brilliant “adaptive camouflage” mechanic. Players control chameleons that must shift their colors and textures in real-time to perfectly blend into their surroundings, turning simple rooms into high-stakes puzzles of stealth. This intuitive, fast-paced design makes every match a tense, hilarious game of cat-and-mouse that is as fun to play as it is to watch.

The Anatomy of a Viral Hit The game’s explosive success is largely driven by its “snackable” nature, which has made it a goldmine for content creators. Because rounds are lightning-fast and filled with “near-miss” moments, gamers on TikTok and YouTube have turned their funniest escapes into viral highlights. These clips showcase players holding perfectly still while a seeker walks right past them, creating a collective thrill that has invited millions of people into the fold. The game’s ability to turn a simple mechanic into a social event has proved that you don’t need a massive budget to create a global gaming phenomenon—you just need a concept that keeps everyone on the edge of their seat.

Navigating the Sea of Clones While the original Meccha Chameleon has reached a massive 15-million-unit milestone, its popularity has triggered an inevitable “gold rush” in the mobile app market. Dozens of unauthorized clones have flooded app stores, all attempting to mimic the original’s art style and gameplay to siphon off its success. While these copycat versions range from simple knock-offs to blatant clones, they stand as a testament to the original game’s massive impact. As players navigate these stores to find the real deal, the original title remains the undisputed king of the genre, continuing to set the standard for what a simple, addictive, and community-driven game can achieve.

🔔 🏛️ The Semiconductor Super-Listing: SK Hynix Moves to Nasdaq

South Korean chipmaker SK Hynix is officially launching its U.S. listing on the Nasdaq today, July 6, 2026, as it seeks to raise approximately $28 billion. The company is offering 17.79 million new shares through American Depositary Receipts (ADRs), with ten ADRs representing one common share. This move is designed to capitalize on the global artificial intelligence boom and represents one of the largest new share sales in history, trailing only the $85.7 billion SpaceX IPO from last month.

The final pricing for the offering is expected to be determined this Thursday, July 9, 2026, with trading scheduled to commence on the Nasdaq on Friday, July 10, 2026. SK Hynix plans to utilize the proceeds from this capital raise to aggressively expand its fabrication capacity in South Korea and purchase advanced manufacturing equipment, such as extreme ultraviolet (EUV) scanners from ASML. Analysts anticipate that the listing will remove the “accessibility discount” for U.S. investors and potentially narrow the valuation gap between SK Hynix and its U.S.-based competitor, Micron Technology.

⚙️ Who Holds the Kill-Switch? The U.S. and Chinese Battle for AI Control

The United States is regulating AI through a highly targeted, decentralized approach that prioritizes national security and corporate innovation over rigid nationwide laws. Rather than passing a single comprehensive federal AI act, the U.S. government relies on a patchwork of state-level rules and strategic executive actions designed to keep American tech labs ahead of global adversaries. For instance, the federal government uses executive orders to require top-tier labs like OpenAI and Anthropic to submit their most powerful frontier models for voluntary cybersecurity vetting prior to public release. This system allows the U.S. to rapidly monitor potential cyber-warfare or infrastructure threats without saddling tech companies with slow, innovation-crushing bureaucratic red tape.

In sharp contrast, China enforces a highly centralized, rigid, and proactive regulatory system controlled entirely by the state. The Cyberspace Administration of China (CAC) mandates that any company developing generative AI or recommendation algorithms must register their training models and pass a strict government review before hitting the market. Instead of waiting for tech to break, Beijing writes specific laws targeting individual use cases, such as strict rules governing deepfakes, algorithmic fairness, and intellectual property. The core philosophy driving Chinese regulation is absolute alignment; AI systems are legally required to uphold socialist core values and refrain from generating content that could destabilize public trust or challenge state authority.

The fundamental clash between these two superpowers boils down to a race between rapid tech dominance and total algorithmic control. While the U.S. framework is reactive and market-driven—allowing tech companies to innovate freely until individual states step in to curb bias or protect data privacy—China’s framework is entirely preventative, ensuring the government holds the kill-switch to any digital tool before it reaches the public. The U.S. relies heavily on export controls to cut off foreign adversaries from accessing advanced American software chips and models, whereas China focuses on building a self-reliant, state-approved ecosystem. This polarization leaves global tech companies caught in the middle, forced to navigate a fragmented digital landscape split between American corporate autonomy and Chinese state compliance.

🚀AI Agent Startups Are Growing Faster Than SaaS Ever Did—and It’s Just Getting Started

AI agent startups are scaling at a speed that traditional SaaS companies never experienced in their early years. Instead of building static tools with fixed workflows, these startups are deploying autonomous systems that can plan, decide, and execute tasks on behalf of users. This shift dramatically reduces the need for manual input, which is why adoption is happening faster across industries like marketing, customer support, coding, and finance. Companies are not just buying software anymore—they are integrating decision-making systems that behave like digital workers.

Unlike SaaS, where growth depended heavily on user training, onboarding funnels, and feature expansion, AI agent startups are benefiting from instant utility. A single agent can replace multiple tools, which increases perceived value and shortens the buying cycle. Businesses are quickly realizing that these agents can reduce operational costs while increasing output, leading to rapid experimentation and fast-scale deployment. This “plug-and-perform” nature is accelerating revenue growth curves far beyond what traditional SaaS models achieved in their first decade.

Investors are now treating AI agent startups as the foundation of the next software revolution. Instead of focusing on dashboards and interfaces, the value is shifting toward intelligence, autonomy, and orchestration. As more companies embed agents into daily operations, a new ecosystem is forming around them—data pipelines, memory systems, and multi-agent coordination layers. This is why many analysts believe AI agent startups are not just growing faster than SaaS ever did, but are actively redefining what software itself means in the modern economy.

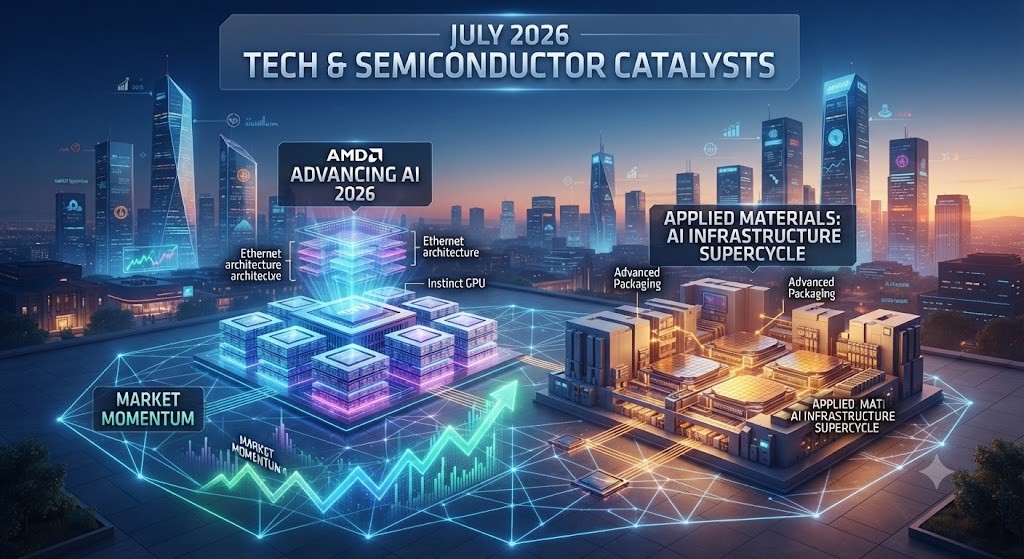

📊 Market Outlook: July 2026 Tech & Semiconductor Catalysts

As we enter July 2026, the technology and semiconductor sectors are entering a “gut check” period. Investors are shifting their focus from pure AI sentiment to tangible ROI, creating unique volatility and opportunity catalysts.

Advanced Micro Devices, Inc. (NASDAQ: AMD): Technology—Semiconductors.

AMD is positioning itself as a primary beneficiary of the “AI infrastructure” pivot, with a significant catalyst arriving mid-month. The stock is currently consolidating as investors prepare for the “AMD Advancing AI 2026” event in San Francisco. This is a major market catalyst where management is expected to unveil new enterprise-grade AI architecture, multi-plane Ethernet infrastructure, and updated deployment strategies for its Instinct GPUs. The market is looking for evidence that AMD can capture market share from dominant incumbents as hyperscalers transition from training models to high-scale inference. Long-term valuation is currently pricing in the transition to “AI factory” architectures, where network efficiency becomes as critical as raw GPU performance.

Applied Materials, Inc. (NASDAQ: AMAT): Technology—Semiconductor Equipment.

Applied Materials remains the definitive “picks and shovels” play for the ongoing AI infrastructure supercycle. Despite a recent pullback that has shaken out weaker hands, the stock remains a focal point for institutional accumulation due to its foundational role in the expansion of foundries globally. The upcoming Q2 earnings season will serve as the primary catalyst. Wall Street is looking for confirmation that the “Capex Supercycle”—projected to reach massive scale—is sustaining its momentum, particularly regarding orders for advanced packaging and high-bandwidth memory production lines. Investors should monitor this for signs that the divergence between semiconductor hardware strength and software-side “spending jitters” continues to favor the equipment leaders.

Strategic Note: The July Earnings “Gut Check”

Market analysts indicate that July will be the definitive test for the “Magnificent 7” and their massive AI spending. If earnings reveal that hyperscalers are slowing data center capex, watch for a secondary rally in semiconductor equipment and component suppliers. When capital is constrained, procurement teams prioritize mission-critical hardware (chips, sensors, memory) to maintain operational capacity, effectively giving these suppliers increased pricing power and defensive stability against broader market volatility.

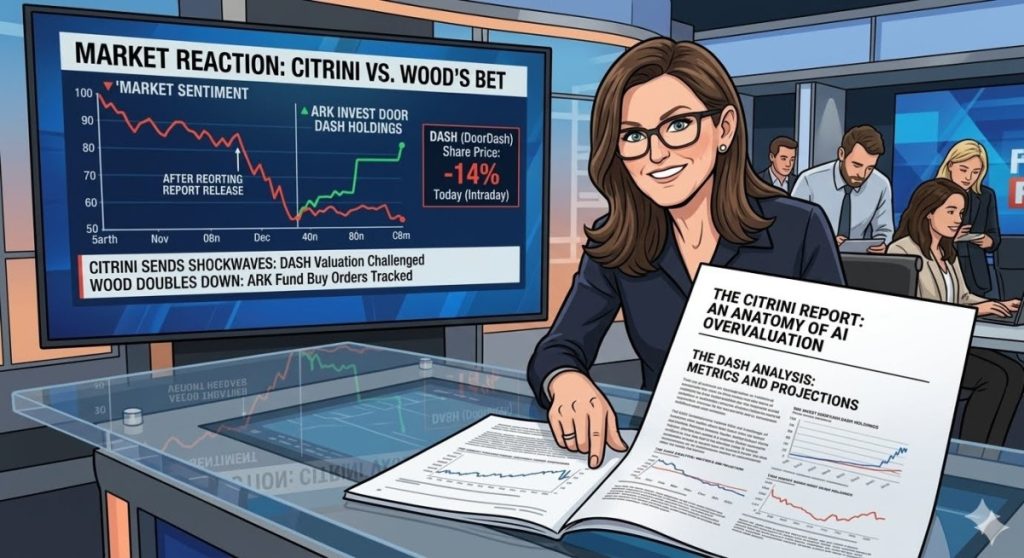

🔥The Anatomy of a Viral Panic: Inside the Citrini AI Report and Cathie Wood’s Big Bet

James van Geelen and Alap Shah wrote a fictional story imagining a scary future where artificial intelligence (AI) destroys the economy by 2028. They filled the report with highly technical financial words to make it feel authentic. The story quickly went viral online, but powerful Wall Street computer programs mistook the fiction for a real-world emergency and instantly began selling off stocks.

This automated computer panic triggered real financial chaos, causing the Dow Jones stock market index to suddenly plunge by 822 points. Investors everywhere panicked as stock prices fell, making many people fear that the fake AI doomsday scenario was actually coming true right then and there.

Famous tech investor Cathie Wood stepped in to stop the panic, arguing that the viral report was completely wrong. She stated that AI will actually cause a massive explosion in business growth and used the market drop as an opportunity to buy up the discounted tech stocks. Her actions helped calm the market, proving how easily viral internet stories can trick computers but also create buying opportunities for humans.

🏦⏳ The $397 Billion Warning: Why Warren Buffett is Hoarding Cash Instead of Buying Stocks

Berkshire Hathaway has reached a historic milestone, reporting a record $397.4 billion in cash and short-term U.S. Treasury bills at the end of the first quarter of 2026. This massive liquidity position, which represents approximately 59% of the company’s total investable portfolio, has continued to grow under the leadership of newly appointed CEO Greg Abel. The accumulation of this “war chest” has been driven by a deliberate and sustained strategy of net selling in the equity markets, as Berkshire has offloaded more than $170 billion in stock over the past several years, significantly trimming core positions like Apple and Bank of America while remaining highly selective with new capital deployments.

Wall Street analysts and investors are deeply divided over the implications of this unprecedented capital preservation. While some view the defensive posture as a pragmatic response to stretched market valuations—evidenced by the “Buffett Indicator” (market cap to GDP) hitting historic highs in early 2026—others express concern that the company’s refusal to deploy capital signals a lack of confidence in current market growth. As Berkshire continues to prioritize the safety and liquidity of short-term Treasury yields over equity risk, the firm remains positioned to capitalize on potential market dislocations, leaving the financial community to debate whether this liquidity reflects a disciplined margin of safety or a tactical preparation for an impending macroeconomic correction.

📉 South Korean Market Meltdown: Tech Panic Triggers Rare Circuit Breakers

In June 2026, the South Korean stock market experienced heightened volatility, triggering emergency circuit breakers on multiple occasions as the KOSPI index faced sharp intraday declines. These trading halts—mechanisms designed to pause activity when an index drops by more than 8%—were largely driven by intense sell-offs in major semiconductor stocks like Samsung Electronics and SK hynix. The market turbulence was fueled by growing concerns regarding slowing global demand for memory chips, potential delays in high-profile tech IPOs such as OpenAI, and fears that the massive capital expenditures required for AI infrastructure might be reaching unsustainable levels.

The frequency of these circuit breakers has positioned the KOSPI as a critical “early warning system” for the global tech sector, as foreign investors rotated out of semiconductor-heavy positions and reallocated capital amid shifting risk appetites. This volatility was further amplified by historic levels of retail leverage and a concentration of index weight in a few dominant chipmakers, making the South Korean bourse particularly sensitive to fluctuations in global AI sentiment. As global markets monitor these developments, the Korea Exchange has held emergency meetings to assess market stability and discuss measures to mitigate the impact of program-driven selling and heightened geopolitical risks.

The Great Tech Rotation: Why Billions Are Fleeing Chip Stocks For AI Software

The stock market is witnessing its most dramatic structural shift of the year as a massive macro capital rotation pulls billions of dollars out of high-flying semiconductor stocks and into deeply discounted enterprise software and healthcare names. This aggressive rebalancing has snapped the momentum of major indexes, leaving the Nasdaq and S&P 500 stuck in their longest consecutive weekly losing streaks since last year. Heavyweights like Broadcom, Micron, and SanDisk have tumbled up to 13% in single sessions over rising fears that hyper-scale AI data center spending is hitting an unsustainable, debt-fueled ceiling.

Conversely, software giants like ServiceNow, Palantir, and Microsoft are skyrocketing as institutional investors aggressively hunt for cheap valuations with highly predictable SaaS business models. This defensive migration is fundamentally altering market leadership, shifting the spotlight from hardware producers to the enterprise applications that deploy artificial intelligence. While chipmakers face near-term valuation compression and normalization risks, the massive influx of capital into the software landscape is engineering a powerful relief rally across tech platforms that had previously bottomed out at 52-week lows.

🚀 BOOM! Micron ($MU) just absolutely crushed earnings and the stock is flying +16% overnight!

If you are looking at your stock app right now and seeing RED, don’t panic—you aren’t losing money! That red color is just a frozen snapshot of yesterday’s regular daytime trading session, which closed down a tiny 0.31% at $1,048.51. Because Micron dropped its blockbuster AI earnings report after the 4:00 p.m. closing bell, the massive explosion in buying is sitting right below the main text in the “After Hours” line. The stock skyrocketed a massive +$165.45 (+15.78%), pushing the real trading price to a wild $1,213.96 per share.

The AI Chip Boom Just Triggered a Massive Stock Rebound! 🔥

The moment the opening bell rings this morning at 9:30 a.m. EDT, the main chart will completely reset, turn bright GREEN, and instantly gap up to that $1,213 level. Micron just proved the AI memory chip demand is higher than anyone expected, blowing past Wall Street’s profit targets and guiding for next-quarter revenue up to an insane $51 billion. Hold onto your shares, because the market open is going to be electric! 📈🔥

U.S. stock futures are soaring as tech giants rally following a blowout earnings report from Micron Technology, sparking an aggressive, sector-wide turnaround. Driven by insatiable artificial intelligence demand and an ongoing memory chip shortage, Micron smashed fiscal third-quarter estimates with revenue that more than quadrupled to $41.46 billion. The stellar result completely reversed a brutal two-day tech sell-off, pushing Nasdaq 100 futures up 1.8% and S&P 500 futures up 0.5%. The optimistic wave cascaded globally, sending South Korea’s Kospi index up over 5% as major hardware producer SK Hynix jumped 12% following a historic U.S. IPO filing.

Beyond hardware infrastructure, broader macroeconomic trends and corporate updates are heavily shifting capital across the market. Energy sector stress eased as Brent crude futures plummeted over 4% to $73.74 a barrel, erasing previous wartime price spikes as shipping congestion clears. Lower energy costs provided immediate relief for transportation stocks like American Airlines, while banking giants caught a powerful tailwind after successfully passing the Federal Reserve’s annual stress test. Concurrently, consumer retail saw bizarre volatility as a massive, retail trader-fueled social media campaign on Reddit sent Wendy’s stock surging 26% to a seven-month high.

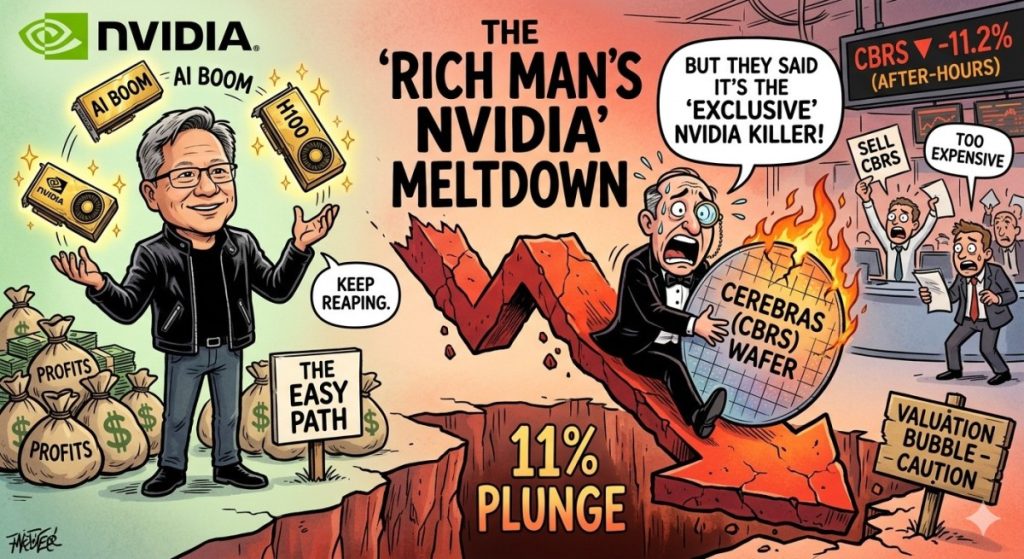

📉 Rich Man’s Nvidia” Meltdown: Why CBRS Just Plunged 11%

Artificial intelligence upstart Cerebras Systems (CBRS) is experiencing an intense post-IPO meltdown, with its stock plunging roughly 11% to $201.55 per share in extended after-hours trading following its first public Q1 2026 Earnings Report.

Despite posting a strong 94% year-over-year revenue surge to $193.4 million and highlighting massive multi-year partnerships with OpenAI and AWS, the stock triggered widespread “AI fatigue” after issuing a severe core gross margin warning. Management forecasted a steep drop in gross margins to between 36% and 38% for the upcoming quarter—down from 46.5%—sparking fears that the company is suffering a brutal margin squeeze as it struggles to source physical data center space.

The sudden overnight crash has turned the ticker into a viral meme on financial forums like r/wallstreetbets, where retail traders are flooded with screenshots of heavy portfolio losses after buying near the stock’s post-IPO peak of $385. Ironically, Cerebras’ actual corporate losses narrowed significantly during the quarter to beat Wall Street targets—meaning the “meltdown” is strictly tied to the cratering stock price and extreme valuation, not the company’s operating performance.

Dubbed the “Rich Man’s Nvidia” due to its massive, single-wafer processing chips, Cerebras is now facing a painful reality check as investors realize that solid revenue growth isn’t enough to sustain its highly inflated valuation. Social media sentiment has rapidly shifted to panic, with commentators warning that the broader AI infrastructure trade may be overheating as physical bottlenecks, like building power and data center availability, limit near-term upside.

🚨SpaceX’s IPO Rollercoaster: Retail Investors Panic as SPCX Hits a Massive Air Pocket.

The record-breaking SPCX initial public offering has completely upended the markets, triggering an unprecedented wave of volatility as retail FOMO battles institutional caution. After pricing at $135 and skyrocketing past $225 to briefly make Elon Musk the world’s first official trillionaire, the stock has encountered heavy turbulence, pulling back sharply into the $154–$170 range. This dramatic correction has ignited a fierce debate across financial forums, dividing traders between those eager to “buy the dip” on a generational aerospace giant and those warning of a speculative bubble driven by pure hype.

Beneath the trading mania, the core drivers of this volatility stem from SpaceX’s aggressive pivot toward AI infrastructure and unexpected corporate maneuvers. The massive $60 billion acquisition of AI coding platform Cursor caught pure-play space investors off guard, while regulatory filings revealed a staggering $12.7 billion cash burn dedicated to building out data centers for xAI. Coupled with deep net losses—including over $4.28 billion in Q1 2026 alone—and a recent Triple-C ESG rating downgrade from MSCI due to governance concerns, the stock is currently acting as a high-stakes battleground for the future of both space and artificial intelligence.

🚨 THE BIG SILVER SQUEEZE IS GAINING MOMENTUM 🚨

While many retail investors remain focused on short-term price swings, a much larger story is unfolding beneath the surface. The global silver market is experiencing its sixth consecutive year of supply deficits, with hundreds of millions of ounces removed from above-ground inventories over that period. Unlike many commodities, silver supply cannot be rapidly increased because the majority of global production comes as a byproduct of mining for copper, zinc, lead, and gold. This means silver output is largely tied to the economics of other metals rather than silver prices alone.

As inventories continue to tighten and new discoveries remain limited, institutional investors are increasingly accumulating silver mining and streaming companies in anticipation of a prolonged supply-demand imbalance that could reshape the market for years to come.

💡 WHY SILVER COULD BECOME ONE OF THE MOST IMPORTANT METALS OF THE DECADE

Silver is far more than a precious metal. It possesses the highest electrical conductivity of any element on Earth, making it indispensable for modern technology. Every solar panel requires silver, advanced semiconductors rely on silver-based components, electric vehicles use significantly more silver than traditional automobiles, and the explosive growth of AI data centers is increasing demand for power infrastructure that depends heavily on silver’s unique conductive properties. Unlike many industrial materials, there are few cost-effective substitutes that can match its performance. As governments and corporations invest trillions into clean energy, electrification, and artificial intelligence, demand for silver continues to climb while supply growth remains constrained. This powerful combination of rising industrial consumption and limited mine production is why many analysts view silver as one of the most strategically important commodities of the next decade, with companies such as Pan American Silver (PAAS), Hecla Mining (HL), First Majestic Silver (AG), and Wheaton Precious Metals (WPM) positioned to benefit if the supply squeeze intensifies.

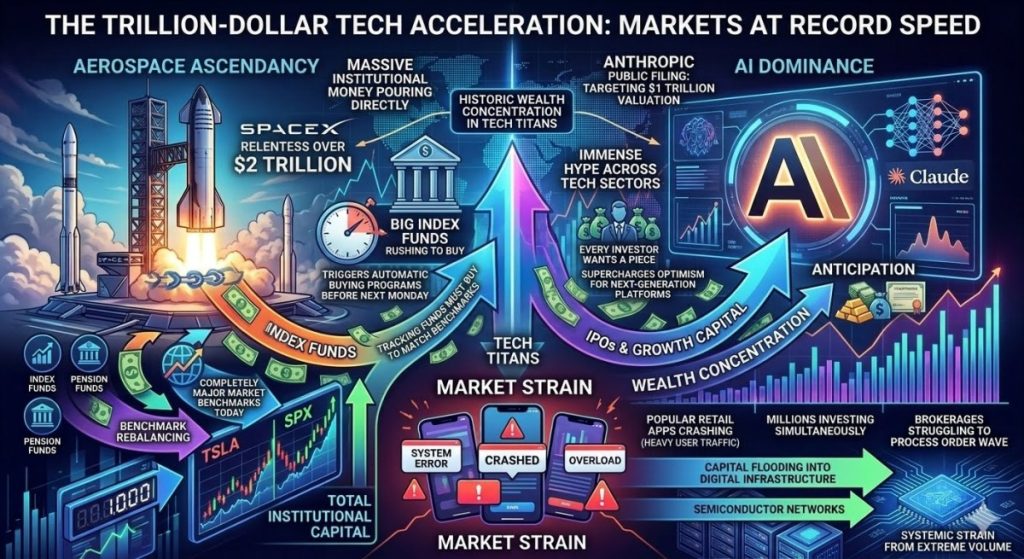

The Trillion-Dollar Tech Boom

The trillion-dollar tech boom is accelerating at record speed. Massive institutional money is pouring directly into SpaceX. Big index funds are rushing to buy the stock. This activity triggers automatic buying programs before next Monday. Tracking funds must buy shares to match benchmarks. This relentless pressure keeps the valuation over two trillion dollars. Large institutions are shifting capital into the aerospace giant. This movement completely reshapes major market benchmarks today.

Artificial intelligence giant Anthropic is fueling the market fire. The company officially filed to go public this week. They are targeting a one trillion dollar valuation. This sudden filing creates immense hype across tech sectors. Every investor wants a piece of this AI leader. The news supercharges optimism for next-generation software platforms. Analysts believe this listing will drive future market growth. The anticipation is pulling money from traditional assets.

This explosive tech excitement is overwhelming global trading infrastructure. Popular retail apps are crashing from heavy user traffic. Millions of investors are buying tech shares simultaneously. This extreme volume breaks previous platform records everywhere. Brokerages are struggling to process the massive order wave. Capital continues flooding into digital infrastructure and semiconductor networks. The market is experiencing historic wealth concentration into tech titans.

📺 THE TV TAKEOVER: How Fox Just Redefined the Streaming War

The acquisition of Roku by Fox creates a distinct competitive advantage by integrating content creation with hardware ownership, specifically through Roku’s established presence in the TV market. While Netflix operates as a self-contained content powerhouse reliant on its subscriber base, the Fox-Roku merger leverages Roku’s significant strength as both an operating system and a manufacturer of smart TV sets. This allows the combined entity to control the entire user experience from the moment the television is turned on, whereas Netflix remains a tenant on third-party hardware.

By owning the screens themselves, Fox is positioned to dominate the advertising ecosystem through deeper data analytics and integrated distribution—a vertical integration strategy that fundamentally differentiates its market position from the platform-agnostic model of Netflix. This move secures control over the platform itself, granting the new entity the ability to leverage first-party data to redefine the advertising experience across the entire streaming industry in ways that a pure content creator cannot replicate.

🚀 THE SPACEX SURGE: History in the Making as SPCX Shatters Records!

The market frenzy surrounding SpaceX (SPCX) has reached a fever pitch, with retail investors and institutional giants alike flooding trading desks to secure a position in what many are calling the most significant IPO of the decade. Across social media and financial forums, the dominant question from investors is no longer if they should enter, but how they can get in before the stock continues its vertical climb. This “SpaceX fever” is fueled by the belief that the company’s dual dominance in aerospace and AI-driven satellite infrastructure represents a rare, generational growth opportunity that transcends traditional sector boundaries.

For those looking to commit capital, the prevailing sentiment is that SpaceX is carving out an entirely new category of value that defies traditional valuation metrics. As the stock continues to sustain its upward momentum, potential investors are aggressively questioning whether the current price point of $192.50 serves as a long-term entry opportunity or merely the beginning of a hyper-volatile phase. The conversation has shifted toward the company’s massive $75 billion capital infusion and its potential to hit $1 trillion in annual revenue by 2030, making it the most sought-after ticker for those aiming to capture the future of global connectivity and extraterrestrial expansion.

⚽ SpaceX Historic $75B IPO Triggers Massive 18% Space Stock Exploded Rally as Global Markets Surge

The global financial landscape is completely dominated by the historic public debut of Elon Musk’s Space Exploration Technologies Corp. (NASDAQ: SPCX). Priced at an unprecedented $135 per share, the monstrous offering successfully raised $75 billion to crown it the largest initial public offering in corporate history, propelling tech index futures sharply higher in overnight trading. This monumental event has unleashed a massive secular rally across the entire space tech sector, fueling immense retail and institutional demand for key infrastructure peers as Firefly Aerospace (NASDAQ: FLY) skyrocketed 17.80%, AST SpaceMobile (NASDAQ: ASTS) surged 11.73%, and Rocket Lab USA (NASDAQ: RKLB) captured heavy pre-market momentum.

Simultaneously, this aggressive satellite and aerospace expansion has been supercharged by an abrupt de-escalation of global geopolitical tensions. Energy markets are reeling after Brent crude futures tumbled nearly 3% toward $90 a barrel following overnight announcements that imminent Middle Eastern military strikes have been entirely called off in favor of higher-level diplomatic resolutions. This sudden macro relief has fueled a powerful risk-on short-squeeze across international equities, sending South Korea’s Kospi index up a staggering 7.8% and Japan’s Nikkei higher by 3.5%, setting up North American space, technology, and defense ecosystems for an explosive opening session.

⚽ 📈 The World Cup Starts Today: The $377 Million Stock Wave You’re Missing.

The kick-off of the 2026 FIFA World Cup today, June 11, serves as a massive macro-catalyst for experiential tech stocks, making Airbnb (ABNB) and Uber Technologies (UBER) the primary equities to watch. According to a Barron’s report on J.P. Morgan data, the tournament will generate roughly $377 million in incremental bookings for ride-sharing platforms. This immediate traffic wave also positions Lyft (LYFT) for highly profitable spillover transit demand. Concurrently, alternative lodging leader Airbnb (ABNB) expects to accommodate over 380,000 international soccer fans. A TIKR corporate analysis notes this event will secure a record-breaking summer print. These severe local supply constraints will undeniably inflate short-term pricing power and platform gross bookings.

Beyond gig-economy giants, traditional lodging and stadium-adjacent food brands require careful tracking. Market experts at Bernstein Travel Research flag Marriott International (MAR) and Hyatt Hotels Corporation (H) as massive beneficiaries. Both companies maintain heavy hotel concentrations across the 16 host cities. For restaurant exposure, a CNBC analysis of Deutsche Bank data highlights key fast-casual winners. Specifically, Sweetgreen (SG) carries a staggering 49% unit exposure to host stadiums. Global footprint brands like Shake Shack (SHAK) and McDonald’s (MCD) will capture significant tourist volumes. Lastly, watch Fox Corporation (FOXA) for multi-billion dollar broadcasting ad revenue gains.

Qualcomm Stock Edges Higher on Blockbuster AI Chip Deal With TikTok Parent ByteDance 🇨🇳

Shares of Qualcomm Incorporated (NASDAQ: QCOM) finished steady on Tuesday, closing up 0.85% at $217.77 USD (+$1.83 USD) following breaking news of a massive cloud infrastructure agreement with ByteDance, the parent company of TikTok. The semiconductor pioneer experienced an immediate surge in buying pressure after reports revealed that ByteDance has officially selected Qualcomm to design the custom application-specific integrated circuits (ASICs) required to power its massive global data center expansions. The strategic partnership represents a major commercial victory for Qualcomm, as its unique chip architectures can be legally supplied to major Asian technology hubs without violating the strict U.S. export restrictions that currently block rival Nvidia from shipping its highest-end artificial intelligence hardware to the region.

This landmark deal effectively transforms Qualcomm’s market narrative, prompting Wall Street to re-evaluate the company as a dominant player in the secular AI infrastructure space rather than just a cyclical smartphone chip supplier. Institutional investors flooded the market with high-volume call options, betting that the ByteDance partnership will spark a significant acceleration in Qualcomm’s higher-margin licensing and hardware revenues. With energy efficiency becoming a critical bottleneck for data centers, asset managers are increasingly rotating capital into Qualcomm, whose specialized chips are engineered to process complex AI inference tasks at a fraction of the power consumption required by traditional, supply-constrained GPU arrays.

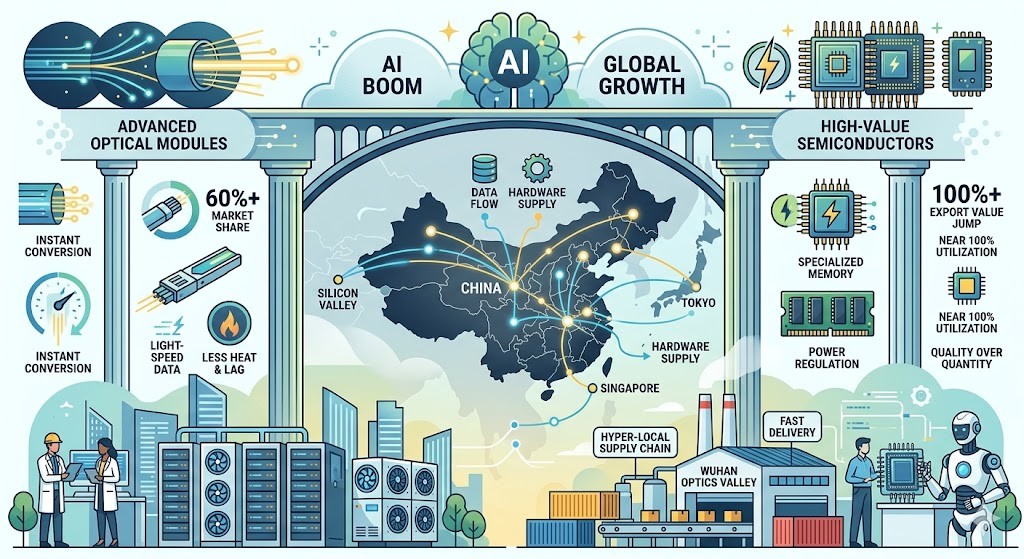

🦾 🇨🇳 The Hardware Backbone: How China Powers the Global AI Boom

China has become the critical backbone for the global AI boom because it builds the physical hardware that runs it. While software gets all the headline attention, tech giants cannot build their infrastructure without the equipment made in Chinese factories. Today, global AI expansion completely relies on this manufacturing pipeline to get the high-speed parts and components needed to keep moving forward.

Inside modern AI data centers, Chinese factories dominate the market for high-speed data connectors. Seven of the top ten companies making these devices are based in China, controlling over 60 percent of the global market. These parts are essential for tech giants like NVIDIA, Google, and Amazon because they use beams of light to send information between thousands of AI chips instantly. This eliminates the slowdowns and intense heat caused by old-fashioned copper wires. Because the race to build AI is moving so fast, factories have sped up their production lines to cut delivery times from 12 weeks down to eight weeks or less.

At the same time, China’s chip factories are shifting from making cheap, basic parts to advanced, high-value tech. This is why recent trade data shows that even though the physical number of exported chips barely grew, the total money made from them doubled to $31.1 billion in a single month. Top chipmakers are running at nearly 100 percent capacity to build specialized memory and power-management chips. These components act as high-tech regulators, keeping massive AI server racks from crashing due to intense power spikes.

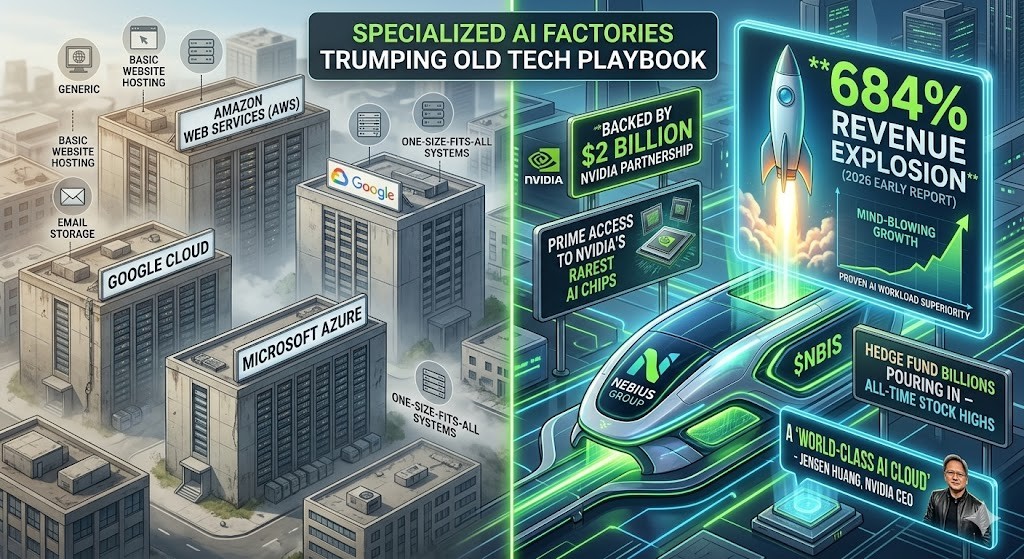

⚡ The Nvidia-Blessed Disruptor: Inside Nebius Group’s ($NBIS) Violent Rise to the Top

Traditional tech giants like Amazon, Google, and Microsoft built their cloud networks to handle everything from basic website hosting to email storage. They are “one-size-fits-all” systems.

Nebius Group ($NBIS) is doing something completely different: they are ignoring the old tech playbook and building highly specialized “AI factories” designed from scratch only for artificial intelligence.

The strategy is working flawlessly. In early 2026, Nebius reported a mind-blowing 684% explosion in revenue compared to last year. This massive growth proves that AI companies are desperate for networks built specifically for their heavy workloads, rather than using old, bloated software systems. Backed by a massive $2 billion partnership with Nvidia, Nebius isn’t just renting out computer chips—they are rewriting the rules on how fast and how cheap next-generation AI can be built.

Nebius is quickly evolving from a basic hardware provider into a true leader of the AI boom. Nvidia’s own CEO, Jensen Huang, recently praised Nebius on the global stage, calling them a “world-class AI cloud.” On top of that, Nebius has been buying up cutting-edge AI startups to make their systems even smarter.

This combination of elite access to Nvidia’s rarest chips and smart technology upgrades has caught the attention of Wall Street’s biggest players. High-profile hedge funds are now pouring billions of dollars into the stock, driving it to all-time highs. Nebius is proving that a fast-moving, AI-first underdog can beat Big Tech at its own game and permanently change the global technology landscape.

Software is dead. Nvidia just built a laptop that doesn’t use apps

Nvidia, in partnership with MediaTek, unveiled the RTX Spark superchip, a 3nm platform combining an Arm-based CPU and Blackwell GPU to deliver 1 petaflop of local AI computing power for consumer laptops. This hardware allows for on-device operation of 120-billion-parameter LLMs, eliminating cloud latency and privacy concerns. Through a partnership with Microsoft, these “Agent PCs” feature the Nvidia OpenShell runtime for secure, native Windows integration to manage complex, autonomous agent workflows. Major manufacturers are developing laptops featuring the chip, including the Microsoft Surface Laptop Ultra, for a Fall 2026 launch. Learn more about the partnership at Nvidia News

💡 Software Shift: How Ask Sage and GenAI Just Rewrote BigBear.ai’s Future

BigBear.ai Holdings Inc. has experienced a powerful resurgence in market momentum, driven by structural operational changes and a notable shift toward higher-value solutions. During its latest financial presentations, the defense and national security specialist highlighted a dramatic gross margin expansion to 34%, a significant rise fueled by an increasing mix of Generative AI product offerings and software integrations like the Ask Sage platform. Although quarterly revenue hovered at $34.4 million, Wall Street responded favorably to the narrowing of net losses and a robust, multi-year contract backlog that has climbed significantly to $385 million, providing a stable foundation for long-term execution.

The enterprise achieved a major commercial milestone by officially securing Panama Transshipment Group as the first flagship customer for its co-developed AI cargo security platform. This critical deployment transitions the firm beyond purely defense-related scripts into tangible global trade infrastructure and logistics, validating real-world enterprise demand for its supply chain security suites. Investors reacted aggressively to this validation, generating strong short-term price momentum that yielded an impressive 27.75% return over a seven-day trading span as the stock pressed upward to trade near the $5.34 mark.

This technical breakout has been significantly accelerated by highly lopsided activity in the derivatives market, where speculative retail participants and institutional buyers have heavily loaded up on near-term positions. Recent data reveals a massive surge in active options trading, with total daily volume hitting 179,660 contracts—an influx dominated heavily by call options, which accounted for roughly 89.43% of the total transactions. With overall open interest climbing past 1 million open contracts and professional day traders closely monitoring positive technical moving averages, the intense call volume concentration has kept near-term buy sentiment highly elevated as the market positions for an ongoing squeeze past immediate resistance levels.

⚡ The Kingmaker’s Endorsement: Marvell’s Trillion-Dollar AI Trajectory

The global technology landscape witnessed a historic market event at the Computex conference in Taipei when NVIDIA CEO Jensen Huang took the stage alongside Marvell Technology CEO Matt Murphy and explicitly crowned Marvell as the world’s “next trillion-dollar company“. This monumental endorsement triggered an immediate, explosive single-day stock surge of over 32%, propelling Marvell’s shares to an all-time record high of $290.79 and injecting tens of billions of dollars of market capitalization into the data center titan in a matter of hours. Wall Street treated the declaration as a validation of a profound structural reality: the emerging era of decentralized AI agents requires localized computational tasks to be aggressively disaggregated and distributed across massive server clusters, rendering high-speed, high-performance connectivity just as critical as raw processing power. By utilizing its industry-leading custom silicon, advanced data center switches, and optical interconnect technologies, Marvell has transitioned from a traditional component provider into an indispensable monopoly anchoring the physical architecture of the global AI supercomputing cycle.

Strategic Dominance and Squeeze Dynamics

This vertical-shifting momentum is heavily reinforced by a profound, multi-billion-dollar corporate alliance, highlighted by NVIDIA’s massive, pre-existing $2 billion strategic equity investment in Marvell to jointly engineer cutting-edge silicon photonics and next-generation telecommunications hardware. Huang’s public validation effectively signaled to global capital allocators that as token generation becomes highly profitable, the hyper-scale cloud providers will expand their capital expenditures exponentially, directly feeding into Marvell’s hyper-growth data center segment which already commands a massive 76% of total corporate revenues. Speculative retail participants and mega-cap institutional funds are aggressively front-running this infrastructure bottleneck, triggering a lopsided influx of call options and lashing a severe technical squeeze against short-term sellers who undercalculated the pricing power of connectivity hardware. While crossing the trillion-dollar threshold requires the company’s valuation to scale multiple fold from its expanded base, the deep algorithmic fusion between Marvell’s data fabric and NVIDIA’s compute dominance has firmly established a new paradigm for the technology bull market.

NVIDIA Shakes COMPUTEX 2026: The Local AI PC and Robotics Revolution 🚀

NVIDIA has fundamentally reshaped consumer computing at COMPUTEX 2026 by moving away from cloud-dependent infrastructure and launching a massive push into local, on-device artificial intelligence. Partnering deeply with Microsoft, the tech giant unveiled the NVIDIA RTX Spark™ Superchip, an Arm-based processor engineered to run complex personal AI agents natively on consumer devices. This powerhouse connects a Blackwell RTX GPU directly to a Grace CPU via NVLink, delivering 1 petaflop of AI compute and up to 128GB of unified memory. Integrated with NVIDIA OpenShell for secure Windows environments, slim laptops from Dell, HP, Lenovo, ASUS, MSI, and Microsoft Surface are scheduled for rollout this autumn.

Beyond personal computers, the architecture shift expands deep into enterprise data centers designed specifically to handle agentic workflows. The newly announced NVIDIA Vera CPU optimizes agent sandboxes and tool orchestration, cutting peak memory latency by 40% compared to traditional x86 processors, while the Vera Rubin System utilizes MVLink72 interconnects for massive rack-scale data processing. Simultaneously, NVIDIA is aggressively scaling its footprint in physical robotics with NVIDIA Cosmos 3, an open frontier foundation model merging visual reasoning and action prediction, alongside the NVIDIA Isaac GR00T Reference Humanoid Robot platform built on Jetson Thor to accelerate global automation development.

🇨🇦🇨🇳 The Tariff Trade-Off: How TD Bank Projects China’s New Capital Will Reshape the North American Corridor

Canada is preparing for a gradual recovery and influx of Chinese investment from a historical low, shifting from state-backed resource mega-deals to a pragmatically driven, transactional relationship. Following Prime Minister Mark Carney’s strategic pivot and Chinese Foreign Minister Wang Yi’s historic visit to Ottawa, TD Bank Economics projects that the total stock of Chinese Foreign Direct Investment (FDI) in Canada could grow to $90–$100 billion over the next five years.

According to the TD Economics Canada-China Report, this base forecast represents an incremental $15 to $25 billion injection of capital directly catalyzed by the newly minted Canada-China Strategic Partnership Roadmap, driving China’s portion of total Canadian incoming FDI steadily back up to its 2019 peak of 5.3%.

The structure of this incoming capital flow differs sharply from past waves, moving away from state-backed entities and heavily targeting specific sectors while adhering to strict federal national security boundaries. Rather than buying out Canadian mining or oil giants, the new momentum is driven by first-time, non-state-owned private enterprises focusing on green partnerships and supply chains. To guide this capital safely, the federal government has clearly bifurcated the Canadian economy, a sectoral risk breakdown that TD Economics highlights as a tight constraint under the Investment Canada Act:

- Approved Growth Sectors: Investment is being funneled into clean energy infrastructure (batteries, solar, wind), EV joint ventures, agri-food, canola, aquaculture, and forestry.

- Strictly Prohibited Sectors: Foreign capital remains tightly restricted or banned from sensitive, dual-use spaces, including Artificial Intelligence (AI), critical minerals, quantum computing, aerospace, and telecommunication networks.

Geographically, this anticipated multi-billion-dollar influx of Chinese capital is highly concentrated across three primary provincial hubs, with distinct regional targets:

- British Columbia (38.2%): Dominating the trade pipeline due to Pacific connectivity, focusing on clean energy infrastructure and forestry.

- Ontario (35.3%): Serving as the primary manufacturing destination for upcoming EV component and battery pack joint ventures.

- Alberta (17.6%): Securing a strong third-place position specifically for conventional energy, agri-food, and modern aquaculture investments.

Despite the optimistic financial projections, this economic realignment faces severe macro friction and geopolitical pushback that could derail long-term stability. Canada’s decision to walk back its previous 100% tariff wall on Chinese clean technology to allow up to 49,000 Chinese-made EVs annually under a favorable 6.1% rate directly diverges from Washington’s protectionist stance. TD Bank analysts explicitly warn that this deeper engagement with Beijing is creating friction with the United States ahead of the upcoming CUSMA/USMCA renegotiations, reinforcing strict natural limits on how far Canada can expand its trade and investment ties without damaging its primary trading relationship.

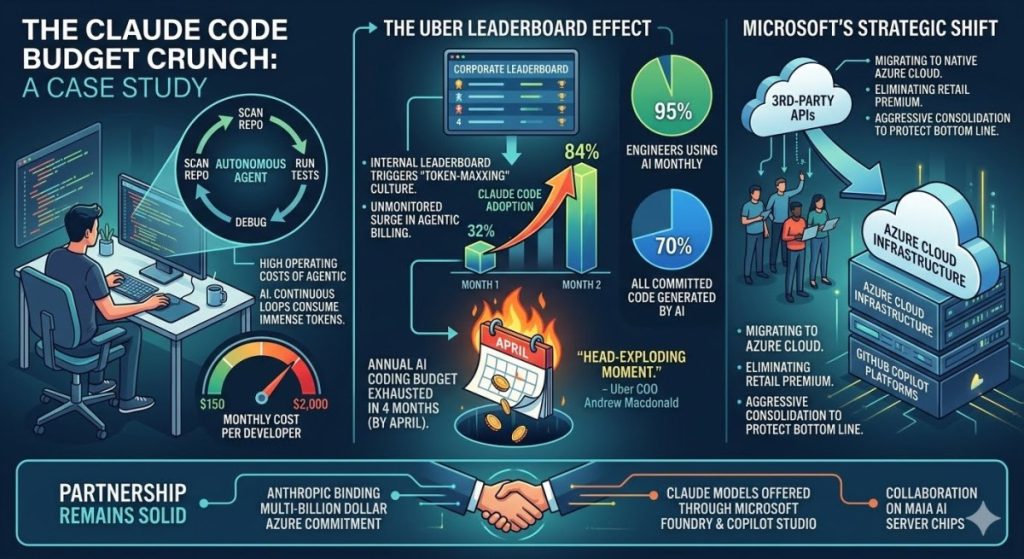

🗑️ ❌ The $3.4 Billion Bill: The Shocking Reason Microsoft and Uber Just Banned Claude